The Fed has inflated the dollar to oblivion since its inception. In fact the 1913 dollar is worth perhaps as much as four cents, which is actually stating that ninety six percent of the dollar’s value has been destroyed. Today, additional money and credit may not be the answer.

The debate over inflation vs. deflation continues and much commentary has been written by well-structured and clear arguments on both sides of the debate. It is a point of fact that most agree that at some point the inflation of the money supply either destroys the currency altogether, where currency basically has no value whatsoever or the currency actually becomes more difficult to obtain and business activity slows down noticeably. In strict parlance there is a contraction in the money supply due to the inability of debtors to service their debt. In plain English the lender does not get their money back. The borrower declares bankruptcy.

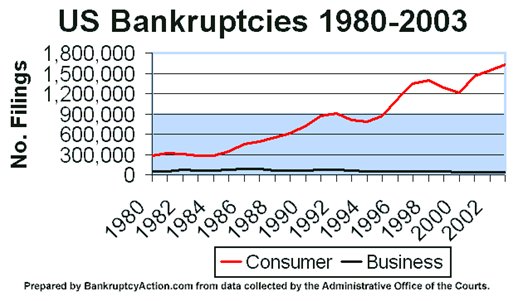

It is interesting to note, bankruptcy filings rose from 1,611,268 in the 12-month period ending March 2003 to 1,654,847 in the same 12-month time period in 2004, according to statistics released by the Administrative Office of the U.S. Courts.

Corporate Bankruptcy

What about corporate bankruptcy? Usually, the stock of a Chapter 7 company is worthless and you have lost the money you invested.

If you hold a bond, you might only receive a fraction of its face value. It will depend on the amount of assets available for distribution and where your debt ranks in the priority list on the first page. If your bond is secured by collateral, your payment will depend in large part on the value of the collateral.

The Largest Bankruptcies 1980 - Present

|

Company |

Bankruptcy Date |

Total Assets |

|

07/21/02 |

$103,914,000,000 |

|

|

12/2/01 |

$63,392,000,000 |

|

|

12/18/02 |

$61,392,000,000 |

|

|

4/12/1987 |

$35,892,000,000 |

|

|

9/9/1988 |

$33,864,000,000 |

|

|

1/28/2002 |

$30,185,000,000 |

|

|

4/6/2001 |

$29,770,000,000 |

|

|

12/9/2002 |

$25,197,000,000 |

|

|

6/25/2002 |

$21,499,000,000 |

|

|

3/31/1989 |

$20,228,000,000 |

|

|

7/14/2003 |

$19,415,000,000 |

|

|

5/13/1991 |

$15,193,000,000 |

|

|

2/8/1990 |

$15,011,000,000 |

|

|

1/22/2002 |

$14,600,000,000 |

|

|

3/7/2001 |

$14,050,000,000 |

|

|

10/22/1992 |

$13,885,000,000 |

|

|

9/20/1991 |

$13,390,000,000 |

|

|

5/8/2002 |

$13,003,000,000 |

|

|

6/12/2001 |

$12,598,000,000 |

|

|

2/28/1990 |

$12,263,000,000 |

|

|

10/1/2001 |

$10,150,000,000 |

|

|

10/31/1992 |

$9,943,000,000 |

|

|

5/30/1991 |

$9,675,000,000 |

|

|

Baldwin-United |

9/26/1983 |

$9,383,000,000 |

* The Enron assets were taken from the 10-Q filed on 11/19/2001. The company has announced that the financials were under review at the time of filing for Chapter 11.

Source: BankruptcyData.com New Generation Research, Inc. Boston, MA

So to overlook bankruptcy is to overlook some important data. It does not prove anything other than bankruptcy exists. The fact to bear in mind is some investors are in fact losing money due to company failures and you want to make certain that you are not one of them! Anyone that experienced their stock or bond investment becoming worthless knows the pain involved and will realize that inflationary pressure did not bail them out.

There are solutions however, the Federal Reserve can and does play favorites. During the Long Term Capital Management debacle the Fed came to the rescue and prevented what could have been a very serious problem for the entire banking system. It is important to point out that this “potential” of a huge bankruptcy does exist and to merely scoff at the argument that a huge contraction in the “money supply” is impossible does not have merit. We simply came too close with LTCM, to state the Fed will never allow it to take place. Our recent experience indicates that the all seeing, all knowing, and ever present Fed may be very busy in the near future. Rescuing the system once does not guarantee it in the future.

Under the monetary control Act of 1980 the Fed can buy any “asset” it wishes to at full face value. So for example, if the XYZ Auto Company is facing bankruptcy due to competition and obligations to its retirees that cannot possibly be met, the corporate bonds might sell at a large discount anticipating that this is a very large credit risk and the bond holders may not get their full payments. Heck they may not get any payments, they might go bankrupt. At the same time the stock of the XYZ auto company slides tremendously as well. But fear not!!

The MCA of 1980 will come to the rescue and the Fed will simply pay full face amount for those worthless bonds, and the pension guarantee corporation will make certain that all retirees will get that handsome check each month.

Is there a clear logical approach to state with certainty that the greatest likelihood is further inflation or deflation? A debt based monetary system has problems from the very inception and Keynes knew this, but stated it did not matter because in the long run we are dead. Mr. Keynes is dead, but his getting rich tactics by going further into debt argument lives on. How you can borrow your way to riches is beyond any reasoning ability of people but certainly well within the capacity of government economists.

What might be considered is what if spending your way into prosperity stopped working one day? Is this even possible? What would it mean?

The title of this article wishes to point out that trying to fix any problem in life by adding to the problem simply does not work. If there is too much credit in the system then adding more credit (DEBT) may not be the answer. Just because this is not the correct solution does not mean that governments would necessarily follow the logic and might easily make the problem worse.

This fact learned through empirical evidence seems to be within the grasp of the general population when it comes to overeating or even in finance on a micro economic level. If a household is too far in debt it may seem that just one more credit card might be the answer but this seldom solves the problem. But governments are not individuals and credit can be created easily, there is no limit to how much credit can be created because it is simply a number there is no value backing the credit supply. One question that needs to be examined might be, is there a limit of credit worthy borrowers? In the example of the over indebted household at what point does the bank say “sorry you cannot borrow any more, your credit line is cannot be increased!

When it comes to finance, the general populace seems to have been conditioned to think that there is just a proper amount of inflation, which is necessary for the economy to function at optimal performance.

At the recent Silver Summit 2 in Coeur d’Alene Idaho I was introduced giving some details of my experience in the aircraft field. Because I am familiar with flying and the associated language, the thought occurred to me that it might be interesting to combine the disciplines of aeronautics and economics together to see if I could build a case for the reader to at least think about the current credit situation.

Flying on the back side of the power curve—or, as it's more aptly termed, "region of reverse command"—is a situation that is familiar to pilots but certainly not the general public. This is a very real situation and it is my attempt to apply this real life principle to helping the reader understand the current economic conditions of the world at large.

Before attempting

to use this analogy it must be explained what is meant by “Back side

of the power curve.” *

As most readers are not pilots this effort may be tough, but it can

be understood. In the most essential form, what it means to a pilot

is that no matter how much more power (throttle- think gas pedal in

a car) is given to the aircraft the situation is hopeless and the

aircraft will stall. A stall is defined as the wing failing to

provide lift and the aircraft becomes unstable and sometimes the

results are disastrous if the pilot cannot execute a stall recovery.

The Fed Throttle

Some of these terms apply to the economy as well as aerodynamics. The occasional reference to the economy “stalling out” is familiar. In fact under the Keynesian economic view all that is needed to correct an economy that is “stalling.’ is for the Fed to “soften” money policy and the economy will recover. This is usually achieved by the lowering of interest rates and it does work for a time. Just like adding power to the aircraft can increase your altitude and provide safety.

However, the economy is now in an interesting situation where more and more debt is needed to create an increase in Gross Domestic Product (GDP). This means more money must be borrowed to produce an increase in good or services of the overall economy.

Certainly the reader might consider that a limit exists in currency debasement as well. For example if you woke up tomorrow to find one of those black helicopters dropped two million dollars in 100 dollar bills in your back yard, you might think wow it is about time and suddenly feel much richer!

Now I can pay off my house and buy that new car, and take a long vacation. However, you suddenly get a phone call and discover your neighbor had the same fortune a couple million in their back yard overnight. In fact that dog gone helicopter money hit the entire nation and that crazy Morgan said it would never happen, what the heck does that guy know anyway?

Would anyone really be any wealthier? No new wealth has been created only claims against the existing wealth. The lenders would suffer greatly however as automobile loans and mortgages were paid off quickly and easily. The lender got a raw deal and is far from being happy.

Let us examine a few things to consider

At what point in the fiat money creation does the market recognize that is it only so much paper and it must be exchanged for something quickly before it is too late?

Another question to ask is at what point does further credit creation cease to work? No matter how much new money is “dropped” into the system the ability of that money to stimulate the economy fails? I just received two million new dollars but so did everyone else, would you bother to pick it up? Would a lender take it as final payment?

These are important questions to me and might be of interest to the reader. In fairness another possibility exists as well and is not discussed very often, Harry Browne brought this to my attention; this is the view that we just muddle along. We get further inflation of the credit supply, the dollar continues to slide in value, people adjust their lives accordingly and nothing really bad or good happens.

The same ups and downs in the economy continue since the world lost U.S. dollar convertibility in 1971. No panic just a slow slide into a lower life style for most and a shift in wealth mostly to Asia. We all just learn to live with it, and life goes on.

Many have stated that this is the real situation and it can continue indefinitely.

My view is different however, most systems have limits and accidents do take place in life, in fact uncertainty is a certainty. Economic systems are not totally predictable because they depend upon that weak and very unpredictable human being. The last accepted time frame for people to overreact happened in early 1980, without the drastic action taken by the Fed at that time, we all might be living different lives

This time is it different, the same or something else? The market will decide and investors should prepare for uncertainty ahead. One of the best places to invest for uncertainty is money real money, gold and silver. Both will do extremely well even if the airplane goes down.

David Morgan

October 11, 2004

David Morgan has a weekly radio show on

the metals at

http://www.netcastdaily.com/fsnewshour.htm, additionally he can

be viewed on eTV at

www.freemarketnews.com

Mr. Morgan writes the Silver-Investor.com Newsletter. This e-mail

newsletter is issued on a monthly basis and includes economic news,

overall financial health of the global economy, and currency

problems ahead. Mr. Morgan reports on both silver and gold. Analysis

is usually top down from the commodity sector to the investment

process. The main focus for readers is to focus on Mining equities

that offer high leverage and substantial capital gains over the next

several years. Reports include current trends, long-term

fundamentals, and specific information required for any investor,

especially the serious silver or precious metal investor. E-Mail Price $99.00 per year or $149.00 for regular posting.

*A Crazy Throttle

Picture yourself turning onto downwind at 100 knots and 2400 rpm

when you discover slower traffic ahead. To maintain altitude and

slow your plane to 80 knots, you reduce power to 2100 rpm and raise

the nose slightly. You're still gaining on your traffic, so you

reduce your speed to 70 knots by further reducing power and raising

the nose a bit higher. If, however, you make a final airspeed

reduction to 60 knots, you might discover that it takes additional

power to maintain altitude. When you need more throttle in

order to fly slower, you've defined the region of reverse

command.

If you attempt to slow still further, you might find that even full

throttle won't allow you to hold your altitude. Even though you're

above stalling speed, you're deep into the backside of the power

curve—and your plane will slowly fall to the ground in a flying

attitude unless you do something about it.

If power less than that which is required to sustain level flight at

existing airspeed is present, an airplane will lose altitude. When

flying on the power curve's backside, airspeed decreases when you

lift the nose, and more power is required for level flight. With

power left constant, the airplane will sink.

Ron Fowler is a lifelong flight

instructor, adjunct professor of aviation at Valencia Community

College, Orlando, Fla., and author of flying texts for Iowa State

University Press, Ames, Iowa, and Aviation Book Company, Seattle,

Wash.